3 Indicators That Can Ease The Broad Market Worries

3 Indicators That Can Ease The Broad Market Worries

Is It Over? 3 ETF Signals You May Use For Confirmation

by Gary Gordon

Is the global economic landscape healing? Far from it. Does that typically signal good things for the U.S. stock market? No... but the U.S. Federal Reserve is extremely likely to keep overnight lending rates near zero for years to come. That discourages saving, yet encourages borrowing for the purposes of consumption and investment. Zero percent rate policy also encourages investors to cast aside huge warning signs that might otherwise drag equity prices into a legitimate corrective phase.

How powerful is the effect of the Fed in the current bull market cycle? The S&P 500 SPDR Trust (SPY) hit an intra-day all-time high of 201.9 on September 19. This exchange-traded tracker for U.S. large caps dropped all the way to an intra-day low of 181.92 on October 15; the 9.9% sell-off just missed the official correction mark of 10%. At the precise moment that this was happening - at a time when the Dow was getting clobbered for 450 some-odd points - out came media reports on recent comments by chairwoman Janet Yellen. She had expressed confidence in U.S. economic growth, even in the face of global economic headwinds. The Dow cut its losses by more than half.

On Thursday, October 16, the markets began free-falling again. The Dow slid 170 points before another media report surfaced. This time, the president of the St. Louis Fed, James Bullard, suggested that the U.S. Federal Reserve should consider extending its bond-buying program ("QE3?) beyond October due to market volatility and worldwide economic uncertainty. Are you serious? How do you go from the transition to normalizing rates in 2015 one minute to considering an extension on emergency level bond purchases the next? That's the Fed, though. And the markets went from losses of 1%-plus last Thursday to flat-lining for the trading session; stocks have been rocketing higher ever since.

In essence, investors have been assured that the Fed will back-stop risky asset investment, regardless of valuations or high profile earnings concerns. In fact, it no longer matters whether or not bellwethers - companies like McDonalds, Coca-Cola, Google, IBM, Verizon - have significant issues. The broader ETF benchmarks like SPY can march forward, as long as there is a belief that the Fed can prevent a nerve-wracking downtrend.

With the S&P 500 climbing back above its 200-day, I have added some "long exposure" via iShares S&P 100 (OEF). Nevertheless, I still have a decent chunk in cash.

What do I need to see before adding more to U.S. stock assets? Here are 3 ETF signals that I am watching:

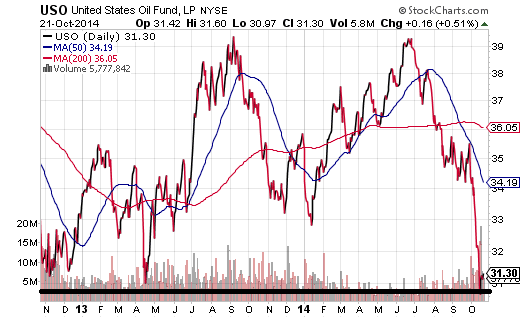

1. Oil via United States Oil Fund (USO). While it is true that consumers and a variety of businesses should benefit from lower energy costs, a lack of stability in the oil markets undermines confidence in global demand. If oil prices do not find a level of comfort - if they continue to slide - investors may fear that the economic slowdown in Europe and Japan will spread to Asia and North America. Moreover, oil at these levels would likely be a net negative to jobs in energy-related industries. In other words, USO better find the kind of support that it did in the latter half of 2012 and the early part of 2013.

USO Daily Chart

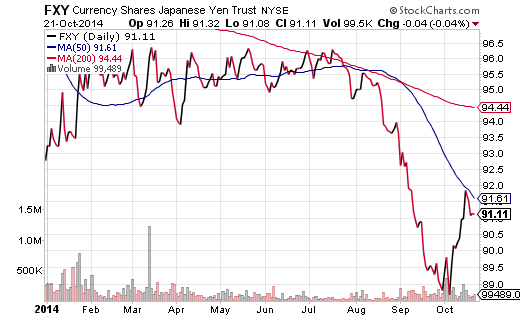

2. Yen via CurrencyShares Yen Trust (FXY). For roughly 15 years, the "yen carry trade" has been a prominent feature of institutional and hedge fund investing. What is it? Investors borrow the low yielding yen to invest in higher yielding assets or higher appreciating assets. Like most things in life, however, there is a down side to the game; that is, if the yen rises in value for its perceived safer haven qualities, institutions and hedge funds rapidly sell stocks, higher-yielding bonds and higher-yielding currencies to avoid paying back loans in the more expensive yen.

Take a look at the momentum FXY had built during the recent corrective activity, literally pole vaulting in the month of October. The yen tracker actually bumped up against its 50-day shorter-term trendline. If the "risk off" correction has truly run its course - if the Fed-fueled "risk-on" mindset is genuinely back on track -FXY will have to stabilize and/or slide. Additional unwinding of the carry trade would likely usher in another bout of heavy volume selling.

FXY Daily Chart

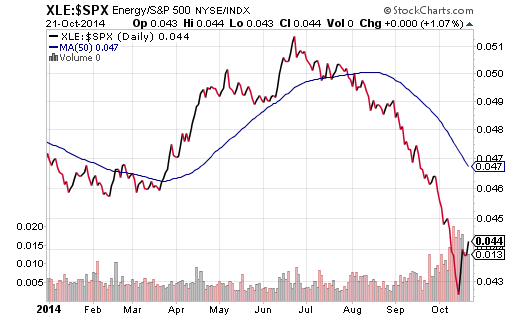

3. Value Investing via SPDR Select Energy Sector (XLE). Admittedly, I am not currently prospecting for "value" in the energy patch. I recently stopped out of 1/2 of client positioning in MLPs and pocketed modest gains. On the other hand, the health of the overall market largely depends on value-oriented mutual funds as well as institutional money managers scooping up price-to-earnings bargains. Since the "traditional" and "fundamental" bargains exist primarily in the energy space - since the energy sector has been hit the hardest since July - a believable stock recovery should see leadership in XLE.

Over the last few days, XLE has shown relative strength in the XLE/S&P 500 price ratio. Bullish investors better hope the XLE:S&P 500 bounce is for real.

XLE/SPY Relative Performance Ratio Chart

Courtesy of TalkMarkets