Is $75 Crude Oil The Tipping Point?

Why '75' Is The Most Important Number For US Economic Hope

by Tyler Durden

US shale oil is now the marginal swing barrel in the new world oil order, and as Goldman Sachs warns (despite Larry Kudlow apparently knowing better), a decline in WTI Crude Oil to $75/bbl would start to significantly slow US shale growth (and thus employment, capex, and the entire US economy).

Via Goldman Sachs:

Our oil forecast calls for a slowdown in US shale oil production which our North American Energy equity research team led by Brian Singer estimates will occur at $75/bbl WTI prices.

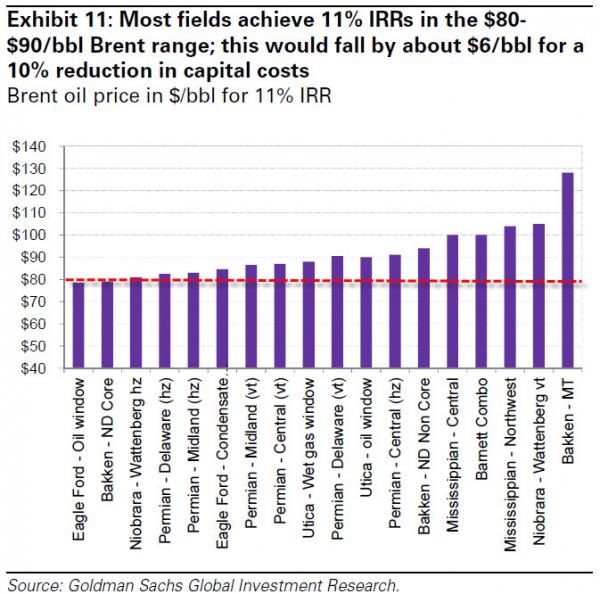

They estimate that the WTI oil price at which average wells in the Eagle Ford, Bakken and Permian Basin plays achieve an 11% IRR (Internal Rate of Return) ranges between $70-$80/bbl. More importantly, they believe that funding gap constraints below $80/bbl WTI will ultimately drive the slowdown in production. Specifically, balancing capex with cash flow is likely to be the key constraint for shale producers, which continue to outspend their cash flow. Historically, E&Ps under our equity research coverage have spent 120% of cash flow annually, with only 2012 above this threshold when several companies which have since changed strategy were large spenders. At our pre-oil price decline capex assumption for 2015, this 120% reinvestment rate would be reached at $80/bbl WTI prices.

Based on their analysis of key shale play production growth at various oil prices, we estimate that WTI prices will need to remain at $75/bbl in 2015 to achieve the required 200 kb/d slowdown in production growth. Given the lag of 4-6 months between when rigs are dropped and when there is an impact to production as well as the impact of hedging, this price forecast implies a larger slowdown in US production growth in 2H15 to 650kb/d yoy.

The uncertainty around this estimate remains elevated nonetheless:

"Some cuts could occur prior to $80/bbl WTI as companies with below-average free cash flow hit reinvestment thresholds first and less well capitalized companies reduce activity. Further, non-core parts of each play have higher breakevens such as non-core Bakken, which represents 19% of total Bakken production and has breakevens above $90/bbl. Finally, the decline rate at major shale plays remains high, potentially exacerbating the production growth slowdown once capex is cut.

Conversely, balance sheets have strengthened over the past few years, leaving less pressure for some companies to cut back on spending during a downturn. Further, these estimates do not assume any service cost deflation that likely would occur in a lower price environment and could lower well costs and the threshold prices at which E&P budgets would fall. Finally, should the global oversupply be significantly larger than we expect, reaching a point of production shut-in would likely require meaningfully lower prices given the low variable costs of shale extraction.

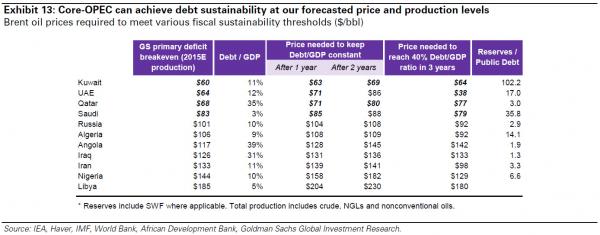

Core-OPEC can cope with lower oil prices

Estimates of breakeven oil price above our 2015 Brent forecast of $85/bbl for many OPEC members raises the question of the fiscal sustainability of these countries.

First and foremost and as we discuss above, cutting production to maintain prices at a higher level is not the optimal (revenue-maximizing) alternative for core-OPEC swing producers, given the current size of shale.

Second, eliminating the primary deficit does not imply debt sustainability as it does not set new debt issuance to zero, but rather equal to outstanding debt service. From a sustainability point of view, what actually matters is not the level of debt, but the relative size of debt to GDP: countries with very low debt-to-GDP ratios might be able to afford running primary deficits for a few periods without compromising their position.

Third, for oil producing countries, a drop in oil prices- all else equal - reduces GDP and raises the debt-to-GDP ratio, potentially adding debt sustainability pressure.

As a result, we consider other breakeven metrics that provide a broader picture and account for these issues. We consider the following simple model across OPEC producers and Russia (RSX): we split the economy into two sectors, oil and non-oil, and let non-oil GDP grow at the going rate while fixing oil production constant at our 2015 expected level. We calibrate the fiscal sector to account for oil and non-oil revenue, expenditures and debt. We then look for: (1) the oil price that lets the debt-to-GDP ratio grow up to 40% over a given number of periods, and (2) how the oil price must evolve to keep the debt-to-GDP ratio constant at its current level. This analysis shows that in both scenarios core-OPEC producers require oil prices that are below our Brent forecast, comforting us in our expectation that they can implement such a change in strategy. In turn, Nigeria and Iran require oil prices well above current levels for either to contain their leverage.

It is worth highlighting that this simple exercise abstracts from FX dynamics as core OPEC members have a pegged exchange rate to the USD. Therefore our breakeven may be an overestimation for countries with a flexible exchange rate, such as Russia and Iran. In particular, Russia's vulnerability to oil prices is lower than for OPEC members given: (1) a flexible ruble that can act as an automatic adjustment mechanism, and (2) a banking sector now in a positive net international asset position, less dependent on foreign funding, and benefiting from a stronger ruble funding base.

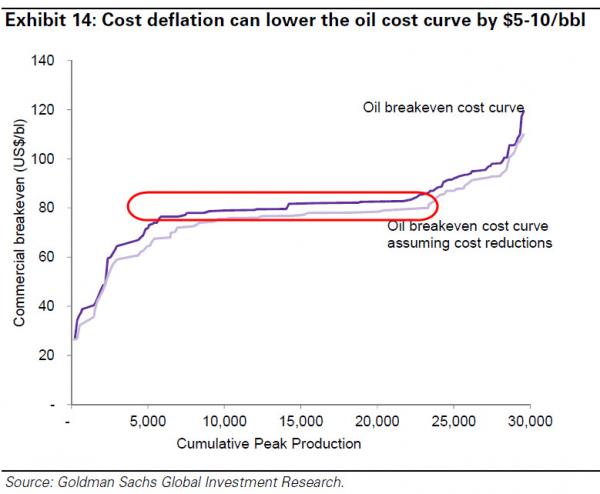

Shale is accelerating the deflation in production costs

We are lowering our long-term Brent oil price forecast from $100/bbl to $90/bbl as we believe that the shale revolution has shifted the global oil cost curve down by $10/bbl. In the next few years, moderate demand growth can accommodate a pull back from more expensive projects. Medium term, continued cost deflation should allow for today's more expensive project to still come online.

Specifically, our European Energy equity research team led by Michelle della Vigna estimates that a slowdown in capex outside North America at a time of material expansion of oil service capacity will lead to a potential 5%-15% cost deflation across oil developments after a decade of 10% inflation. The oversupplied market that we forecast for 2015-16 is likely to lead to a curb in activity that is likely to accelerate these deflationary forces."

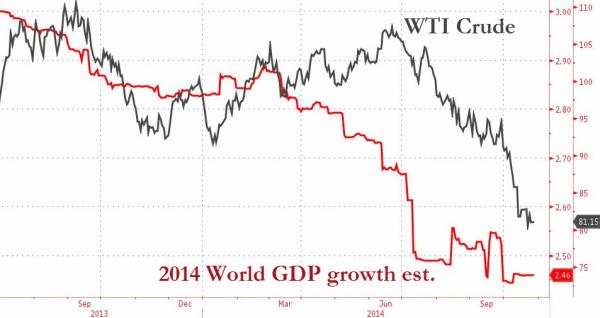

And just one more thing... for those that shun 'demand' weakness as a reason for the plunge in oil...

Courtesy of zerhohedge.com