Why stock-market investors should embrace a flattening yield curve-for now

- Final years of bull market often provides biggest returns -

By Anora M. Gaudiano, MarketWatch

Stock-market investors are nervously watching the Treasury market for a recession warning signal. But even if it comes, history suggests they might not want to be too hasty in ditching stocks.

The yield curve, as measured by the spread between 10-year and 2-year Treasury yields, has been flattening since 2011, when it peaked around 290 basis points, or 2.9 percentage points. On Tuesday, the spread was at 53 basis points.

A flattening of the curve is usually the result of a faster rise in yields on the short end or a faster decline on the long end of the yield spectrum. The most recent flattening of the yield curve is due to the former.

The 10-year Treasury yield rose about 50 basis points over the past 12 months as the economic outlook improved. However, at 2.85% it is below its 2014 peak of 3%.

Meanwhile, the yield on the 2-year Treasury note rose 100 basis points over the same period to 2.27%, its highest level since 2008.

At the late stages of an economic cycle, when the economy is improving rapidly, the Fed often raises interest rates aggressively to control inflation. But that can choke the economy, causing a recession, something that the current Fed is trying very hard to avoid.

An inverted yield curve-when the 2-year yield trades above the 10-year yield-has preceded all five of the past recessions. A different measure-an inversion of the 3-month T-bill/10-year Treasury note spread-has preceded all seven of the past recessions, according to the Cleveland Federal Reserve Bank, with two false positives-an inversion in late 1966 and a very flat curve in late 1998.

But the lag between when the 2-year/10-year curve flattens to 50 basis points and when it inverts-if and when it does-can be long.

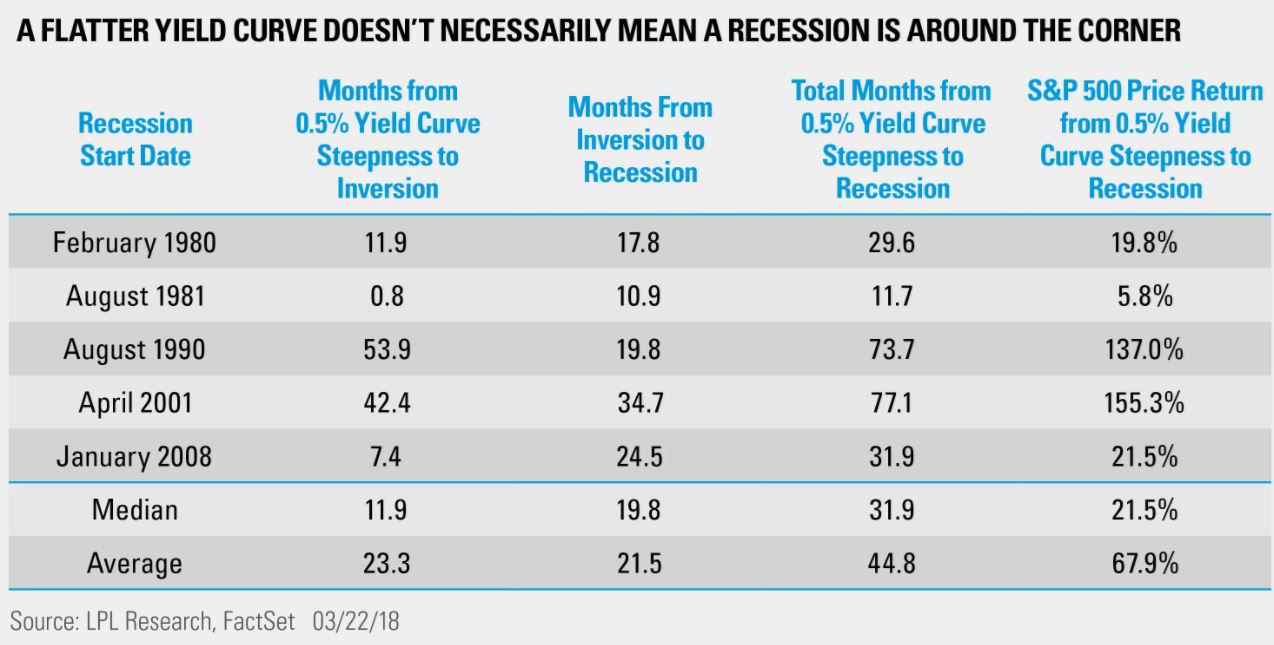

Ryan Detrick, senior market strategist at LPL Financial, looked at the previous five recessions and found that it took nearly a year for the curve to invert once it hit 50 basis points, though the stretch ranged from just under a month to 4 1/2 years.

"Once it inverted, it took about 20 more months until a recession started. All along the way, the S&P 500 posted a median return of 21.5% over those 32 months," Detrick said, in a note (see table below).

In other words, a flattening or inverted yield curve doesn't mean a recession will start tomorrow, according to Detrick.

Meanwhile, the stock market return in the final years of the bull market tend to be the strongest.

Fundamentally, there are reasons for bulls to look for further stock market gains.

"Don't forget we are looking at record profits and revenues for the S&P 500 in 2018 amid multidecade highs in manufacturing and services, along with soft data indicators such as consumer confidence," Detrick said.

"In other words, the economy is still on quite firm footing, and we see few reasons to expect a recession over the next 12-18 months," he said.

From MarketWatch