Will Value Stocks Continue To Outperform Growth Stocks?

Can value stocks keep outperforming growth in second quarter?

Rotation into fundamentally undervalued shares picking up steam

The pendulum is finally swinging back toward value stocks.

It might be too early to call it a comeback, but value-focused investors are ending the first quarter with reason to cheer.

Growth stocks have ruled the roost since well before the bull market that began in 2009. But value stocks, shares that are viewed as undervalued relative to their fundamentals, have outperformed their growth counterparts over the first quarter of this year.

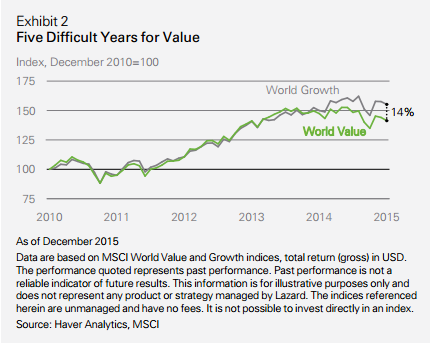

The Vanguard Value Index exchange-traded fund (VTV) is posting a cumulative quarterly return of 2% versus 0.6% for the Vanguard Growth ETF (VUG) (see chart above). In 2015, the growth ETF returned 3.3% versus a 0.1% decline for its value counterpart. In fact, value has underperformed growth for nearly a decade, but value has particularly suffered over the last five years (see chart below), observed Jason Williams, portfolio manager analyst at Lazard Asset Management, in a recent note.

Optimism toward value strategies is on the upswing. A March 12 cover story in Barron’s, for example, declared value stocks poised to take the baton from growth shares.

Value’s underperformance has come as investors instead favored “quality, growth and low-volatility stocks, which has driven strong performance from momentum strategies,” Williams said.

But jitters about the ability of momentum strategies, in particular, had led some analysts last year to ponder whether a style switch was in store. Momentum strategies rely on loading up on stocks that are on a hot streak and, potentially, shorting stocks that have turned cold. That approach has been quite profitable over the course of the current bull market, becoming perhaps the dominant investing strategy.

But soaring valuations for a handful of momentum stocks, particularly the so-called FANG stocks—Facebook Inc. (FB), Amazon.com Inc. (AMZN), Netflix Inc. (NFLX) and Google parent Alphabet Inc. (GOOG) — led to fears the approach had become overstretched.

Equity strategists at J.P. Morgan earlier this month noted the rotation away from momentum into value and said the move could persist for a number of reasons, including the fact momentum shares have traded at an “extreme premium” to value stocks and worries that momentum had become “crowded while value offers greater opportunity.”

They also pointed to macroeconomic trends that could keep driving the rotation, many of which are still intact:

|

"slower U.S. growth and increased volatility resulting in a more dovish Fed; flat-to weaker [U.S. dollar]; stable-to-rising commodity prices including oil (with [commodity trading advisers] still very short and representing 20-40% of WTI open interest); more policy stimulus and improvement in China; commodity induced inflation surprise (even with Fed hiking) would be a positive for Value (including Financials); further stabilization in manufacturing sector (or convergence between goods producing and services industries); further improvement in the 2nd derivative of our business cycle indicator which just turned positive from low levels and moved into Recovery state…); more synchronized business cycles across regions." |

In his note, Lazard’s Williams observed that value had seen its reputation for preserving capital eroded. A lack of “truly cheap stocks” over the last decade also offered a headwind for value investors.

That’s changing, he noted, with some groups, including banks, oil and gas and basic resources, now trading at big discounts to book value.

So it might be early to crow, but value investors can’t be blamed for feeling like they’ve finally started to gain some, well, momentum.

Courtesy of marketwatch.com